02.29.2024

Year in Review: 2023

Year In Review: 2023 Canadian Market Valuation Summary

Introduction

The year 2023 has marked the first year since the pandemic that the automotive market has begun to return to normal. In the second half of the year, it became more common to hear of new vehicle inventories growing and wholesale values declining, bringing back regular levels of depreciation and a return to a more traditional inflation rate, slipping to 3.4% in December.

Used Retail Market

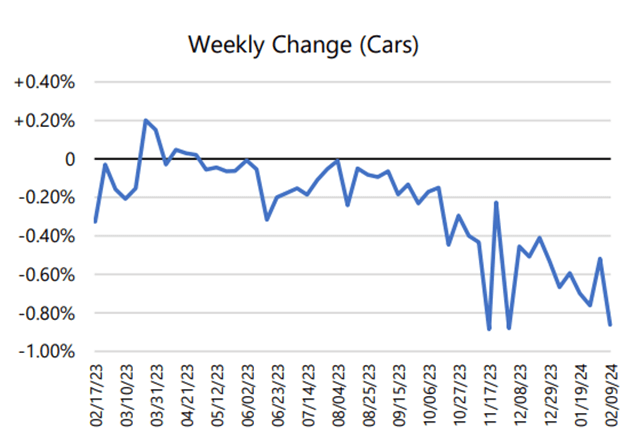

As vehicle export activity slows and interest rates rise, the once-high demand for Canadian vehicles has diminished, leading to a cooling of used market prices. Coupled with the resurgence of new car sales incentives, the industry is moving towards a pre-pandemic state. In 2023, Passenger Cars saw a value drop of 10.9%, while Crossovers and Trucks declined by 22.8%, with most of these losses happening in the final quarter. This represented the first major wholesale market correction and downturn in Canada since before March 2020, a correction deemed necessary to address vehicle unaffordability.

With high interest rates, Canadians are thinking twice before buying new cars. The Bank of Canada is working hard to keep prices stable, which means people are being careful with their money. They are either buying out a current lease, servicing an older vehicle, or altogether delaying their search until variables on affordability come back within range. With the late changes in 2023, many of these obstacles are now starting to break down.

As we approached the middle of 2023, the Canadian automotive industry began to experience a notable decrease in the wholesale market, predominantly affecting the truck segment and larger crossover vehicles. This downturn extended across these larger vehicle categories as the year progressed into the late summer months. In contrast, the market for passenger cars remained comparatively resilient during this period, buoyed by their greater fuel efficiency and affordability, registering a modest wholesale reduction of 5.1 percent relative to the 12.4 percent observed in crossovers and trucks.

The landscape shifted notably with the advent of the fourth quarter. A comprehensive adjustment of previously inflated vehicle values was observed across all sectors. This was attributable, in part, to a retreat in purchasing by U.S. buyers and the concurrent influx of new vehicle stock, which began to permeate the dealership networks in greater volume.

New Retail Market

In the previous year, the Canadian automotive industry demonstrated a significant uptick in new vehicle sales, culminating in an 11.8% year-on-year increase with a total of approximately 1.664 million units sold nationwide. This surge in sales volume, underpinned by a robust rate of growth and bolstered by new car production, bodes well for expectations of continued expansion into 2024.

The retail network’s reaction to the escalation in new car manufacturer’s suggested retail prices (MSRP) is indicative of a pent-up demand that has accumulated over the preceding three years. It is also pertinent to highlight the demographic influence of immigration, with Canada welcoming a record-breaking influx of approximately 1.2 million individuals within the last fiscal period.

Amidst the growing car market, the stabilization of new car pricing has been observed, with an average MSRP increase of merely 10% in 2023. Analysis of retail listings data indicates the average newly listed vehicle was priced at $59,635 over the course of the year. Notably, the price trajectory across various car segments has varied, with a discernible discontinuation of smaller, economical models in favor of the introduction of sub-compact yet comparatively more expensive crossovers. This pricing dynamic is further accentuated by the entry of battery electric vehicles (BEVs), which tend to scale the upper tier of their respective market segments in terms of price. This has contributed to an average MSRP increment of approximately 28% for passenger cars, whereas crossovers and trucks have seen an average increase of 8% compared to the previous year.

This altered pricing structure has directly influenced the promotion of incentives on new vehicle purchases, as the industry attempts to mitigate the combined weight of elevated price points and rising interest rates, striving to offer monthly payment options that are palatable to the consumer. Current observations indicate an average incentive offering of around 7%, a marked hike from the previous lows of approximately 2%.

Concurrently, the escalating cost of new vehicles has significantly influenced consumer leasing behavior, leading to a discernible decline in lease penetration rates. The current trend is a lease penetration consistently registering below 20%, with a notable shift whereby many former leaseholders have opted to transition into cash purchases, particularly within the luxury vehicle market.

Residual Value Forecasting

The landscape of the Canadian automotive industry in 2023—albeit still subject to the fluctuations of a volatile market—exhibited a return to more conventional levels of vehicle depreciation. This reversion constituted a counterbalance to the atypical vehicle appreciation observed in the preceding years of 2021 and 2022. Reflecting these dynamics, our Residual Value projections, calculated on 48-month terms, indicated an average decline of 2%, influenced primarily by wholesale trends throughout the year.

An analysis of segment-specific depreciation reveals that car categories have sustained stronger wholesale values, with an average depreciation of merely 1%. Conversely, the crossover and truck segments experienced a greater average decline of 3%. It is important, however, to contextualize these figures within the environment of the significant valuation increases that the market has undergone in recent years; this means that residual values remain favorably high.

We’ve observed some strategies in association with strong Residual Values this year. In the wake of looming used car supply shortages, some manufacturers have enforced plans to help build up early vehicle returns. Hoping to compensate for a lack of new vehicle sales in recent years, as well as an effort to overcome monthly payment shock. Although these initiatives may yield short-term benefits, they potentially introduce increased risk by accentuating volatility in the residual values of shorter-term leases, particularly those ranging from 12 to 30 months.

Alongside these targeted strategies, 2023 has also seen the introduction of more aggressive sales incentives. Utilizing tools like our Pulse product and retail listing data to monitor ‘Days to Turn’ and ‘Days Supply’ metrics, we have gleaned insights into the rate at which new inventory has accrued and its geographical distribution. Despite intermittent disruptions, such as the labor strikes by UAW and Unifor, which obscured the broader market narrative, it became apparent that specific market segments required enhanced support to facilitate the movement of the increasing new vehicle stock. Consequently, direct consumer incentives—or ‘cash on the hood’—resurfaced, signaling areas of the market more susceptible to significant depreciation.

The electric vehicle (EV) segment, despite an increase in product offerings, did not witness proportionate demand growth. In 2023, the market for full battery electric vehicles contended with subdued interest, which could attributed to the persistent challenges associated with EV charging infrastructure and the overarching issue of vehicle affordability. As market leaders in the EV domain made pricing adjustments, the market responded with rapid and considerable shifts in wholesale valuations, precipitating a decline in what had been strong retention of value for these vehicles.

Zero Emission Vehicles

As the focus intensifies on Zero-Emission Vehicles (ZEVs), the year 2023 marked a significant milestone in the pursuit of Canada’s ambition to transition to a fully ZEV landscape by 2035— A mandate that late in 2023 became legislature at the Federal level. ZEVs have now ascended to represent approximately 10% of all new vehicle sales within the nation, signifying a critical halfway point to the initial benchmark set for 2026.

The prevailing sentiment suggests that the market may have reached an inflection point with early ZEV adopters during 2023, emphasizing that engaging the early majority presents a formidable challenge for the battery electric vehicle market. Simultaneously, the general improvement in the supply of new vehicles has been paralleled by increased production of ZEVs. However, the anticipated surge in demand for these vehicles has not materialized over the past year as expected. This is mirrored in the significant pricing adjustments undertaken by several manufacturers, which appear to be in competitive contention to either bolster or preserve their respective market shares.

This has put downward pressure on wholesale pricing, as the market fights to keep up a with turbulent pricing environment that fosters heightened unpredictability in the valuation of electric vehicles.

Moreover, the introduction of new electric vehicle startups in 2023 suggests a promising maturity within the EV market segment. Established industry participants are observing these market entries with scrutiny, and it is projected that such influxes will precipitate continued price volatility in the near future.

Conclusion

Twelve months after the budding resurgence within the automotive sector, the landscape has evolved considerably. Automobile manufacturers have redoubled their efforts, reintroducing incentives as a strategic measure to expedite the turnover of the growing inventory.

Electric vehicles, once scarce commodities, are now increasingly visible, appearing in dealership showrooms with a greater presence. Market dynamics now enable both new and pre-owned vehicles to be acquired at transaction prices that fall below their initial advertised values. The venerable saying “what goes up, must come down” seems particularly relevant to the current state of affairs in the automotive realm. Oh, what a difference a year makes.

Daniel Ross, Senior Manager, Industry Insights and Residual Value Strategy

Posted in: Dealers